The Hidden Debt Trap in Solar Plant Financing

The commercial and industrial PV financing market is booming, However, many investors find that their actual returns fall far short of expectations and, in some cases, become trapped in hidden debt structures, leading to long-term capital lock-in.

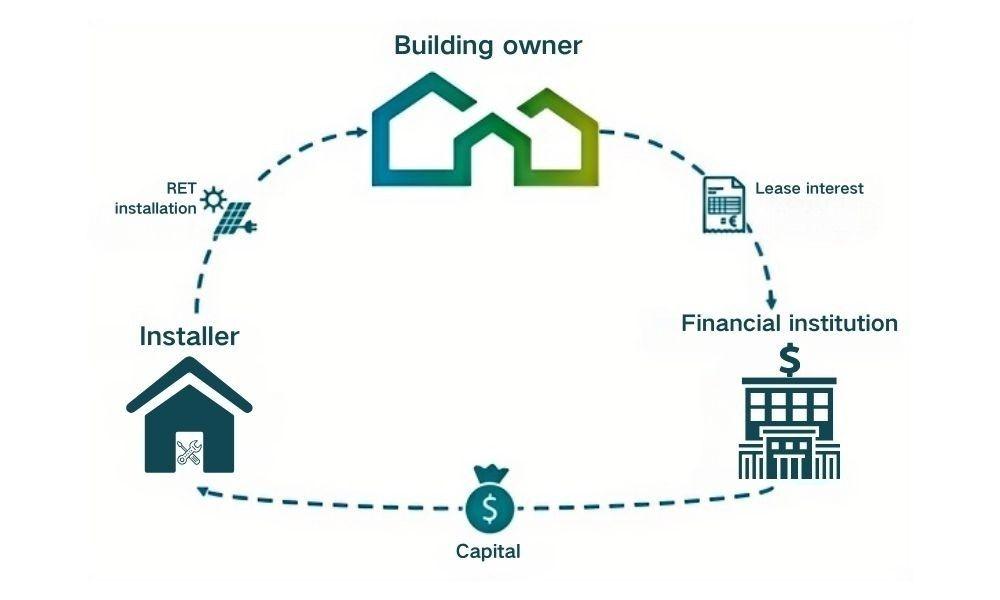

Leasing Model

How It Works

A leasing company purchases PV equipment and leases it to the owner, who makes installment payments over time.

Perceived Advantages

Reduces the owner’s upfront investment and financial burden.

Hidden Risks

Higher financing costs: Lease rates may exceed traditional bank loan rates, leading to underestimated capital costs.

Ownership ambiguity: Disputes often arise over asset ownership and post-lease operational responsibilities.

Risk transfer clauses: Some lease agreements include "recourse clauses," shifting unexpected financial risks to the lessee.

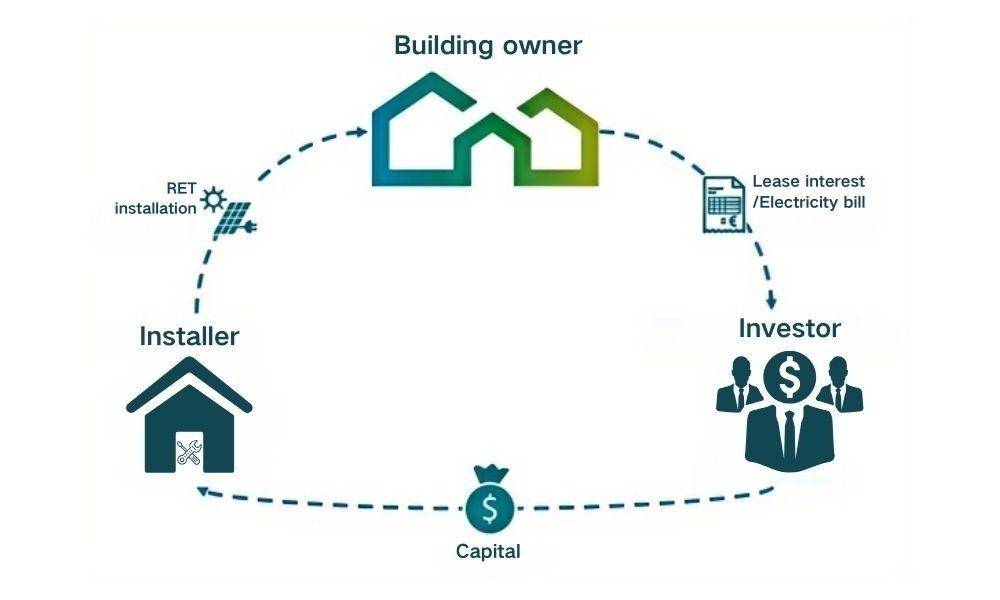

Operational Lease Model

How It Works

Investors finance and build the PV plant, while the owner pays electricity fees or rent; the investor retains ownership of the power plant.

Perceived Advantages

Owners avoid operational risks, while investors receive long-term stable returns.

Hidden Risks

Revenue uncertainty: Investors face risks from fluctuating electricity prices and lower-than-expected power generation.

Policy risk: "Guaranteed return" clauses may become invalid due to subsidy cuts or tariff reductions.

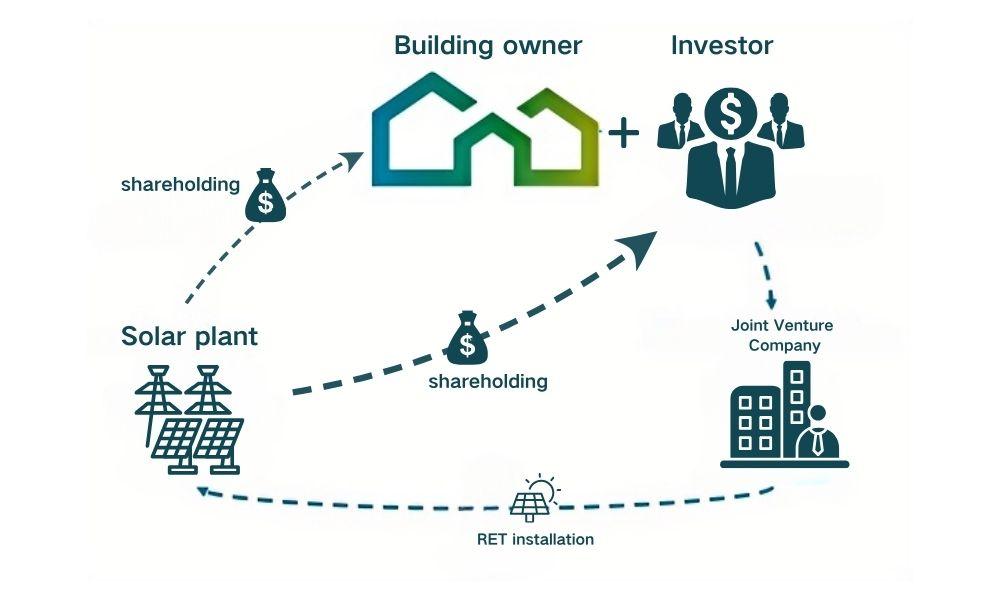

Equity Partnership Model

How It Works

Investors and owners establish a joint venture, sharing profits according to equity ratios.

Perceived Advantages

Shared benefits and risks, seemingly fair and balanced.

Hidden Risks

"Hidden debt" trap: Investors appear to be shareholders but may bear fixed-return obligations, effectively acting as creditors.

Additional capital injections: If the plant underperforms, investors may be forced to inject more funds or absorb losses.

The Illusion of IRR: Why Projected Returns Fall Short

How IRR Models Are Over-Optimized

Overestimated generation output: Ignoring shading, module degradation, and real-world inefficiencies.

Underestimated O&M costs: Failing to account for long-term maintenance, repairs, and cleaning expenses.

Neglecting policy risks: Overlooking subsidy reductions and electricity price adjustments.

Real-World Case Study

A commercial PV plant projected a 12% IRR, but actual operations yielded only 6% due to lower-than-expected power generation and higher maintenance costs.

How Investors Can Avoid Financing Pitfalls

Scrutinize Key Contract Terms

Return Clauses: Differentiate between "expected return" and "guaranteed return" to clarify profit distribution mechanisms.

Risk-Sharing Clauses: Define liability in case of underperformance to avoid "hidden debt" obligations.

Exit Mechanisms: Ensure clear exit strategies to prevent capital lock-in.

Conduct Independent Due Diligence

Generation Forecasts: Require third-party simulations, focusing on shading analysis and degradation factors.

Cost Calculations: Incorporate O&M, financing costs, and policy risks into financial models to avoid overly optimistic projections.

Choose Reliable Partners

Financial Institutions: Prioritize banks and leasing firms with proven PV project experience; avoid shell companies.

EPC Contractors: Work with accredited EPC firms with a strong track record to ensure quality project execution.

Golden Rules for PV Power Plant Financing

- Rule #1: Don't be misled by high IRR figures—develop your own financial model.

- Rule #2: Carefully review contract terms to avoid hidden debt traps.

- Rule #3: Partner with experienced and qualified firms to minimize project risks.

By following these principles, investors can navigate the complexities of PV financing and secure sustainable, profitable investments.